In the popular vote on June 18, 2023, voters welcomed the implementation of the OECD/G20 project on minimum taxation with 78.5 percent voting in favour and 21.5 percent voting against. Voter turnout was 42.4 percent.

Brief summary

Switzerland, along with around other 140 countries, has acknowledged that large multinational enterprises should pay at least 15% tax on their profits in each country. In future, if a corporate group pays less tax in one country, it can be taxed by other countries until the 15% is reached. This concerns large multinational enterprises with an annual turnover of at least EUR 750 million. This is estimated to be a few thousand companies, although there is not enough data to allow a more accurate calculation. All other companies are unaffected.

The minimum taxation project was set up by the Organisation for Economic Co-operation and Development (OECD) and the Group of Twenty major developed and emerging economies (G20). The aim is to adapt the tax rules for large corporate groups to the digitalisation and globalisation of the economy.

The Federal Council and Parliament want to be able to introduce the minimum tax rate by 2024, and thereby create stable framework conditions and secure both tax receipts and jobs in Switzerland.

The minimum tax rate is to be implemented in Switzerland by means of a supplementary tax. This covers the difference between the effective tax rate in the canton concerned and the 15%. The receipts from the supplementary tax are to go to the cantons (75%) and the Confederation (25%). They will then be redistributed between all cantons via the national fiscal equalization system. In this way, financially weak cantons will also receive a portion of the receipts.

It is estimated that the receipts from the supplementary tax will amount to CHF 1-2.5 billion in the first year. However, it is difficult to gauge either the short- or the long-term financial impact of the supplementary tax.

Parliament wants to be able to introduce the OECD minimum tax rate in Switzerland. A bone of contention was the distribution of the receipts from the supplementary tax between the Confederation and cantons, and between the cantons themselves. A minority wanted to grant the Confederation more than 25% of the receipts and to distribute the receipts more evenly between the cantons. This would have additionally dampened the tax competition between the cantons. The Confederation would have been able to invest its higher share of the additional receipts across the whole of Switzerland, for example in measures to increase employment incentives. The chosen distribution ratio led a minority to reject the proposal. However, the majority of parliamentarians want to be able to introduce the OECD minimum tax rate in Switzerland and are in favour of the proposal.

The Federal Council's and Parliament's arguments

Securing stable framework conditions

By implementing the OECD/G20 minimum taxation project, Switzerland is securing internationally stable framework conditions for Switzerland as a business location. Since the affected corporate groups will have to pay the tax in any case, the supplementary tax ensures that tax receipts stay in Switzerland, rather than flowing abroad.

Broad-based compromise

All parliamentary groups are, in principle, in favour of implementing the internationally agreed minimum tax rate. The distribution of the supplementary tax receipts between the Confederation, the cantons and the communes is based on a compromise negotiated by representatives of those entities.

The whole of Switzerland will benefit

The chosen distribution ratio allows the supplementary receipts to be used predominantly where the additional tax burden impinges most on locational appeal. Switzerland as a whole will benefit from the maintenance of locational appeal and the retention of jobs.

Equalization between the cantons

National fiscal equalization ensures that all cantons benefit from the supplementary tax receipts. The higher the cantonal share in these receipts, the higher the amount of funds flowing to the cantons under fiscal equalization. The chosen distribution ratio thus also benefits the financially weaker cantons.

Implementation based on federalism

The proposal respects federalism. For example, the cantons enforce the regulations via the supplementary tax. They are, in principle, free to decide how to use their receipts, but must take appropriate account of the communes.

The Organisation for Economic Co-operation and Development (OECD) and the Group of 20 major industrialised and emerging market economies (G20) want to adapt the rules on the taxation of large corporate groups in line with the digitalisation and the globalisation of the economy. Together, they adopted a corresponding project in October 2021. According to this, large multinational enterprises should have to pay at least 15% tax on their profits, regardless of their location (minimum taxation).

Switzerland has signed up to this project together with around 140 other countries. The Federal Council and Parliament want to be able to introduce the minimum tax rate by 2024, and thereby create stable framework conditions and secure both jobs and tax receipts in Switzerland.

In December 2022, the National Council and the Council of States approved the proposal for the implementation of the OECD/G20 minimum tax rate. In the National Council, it was approved by 127 votes to 59, with 10 abstentions, and in the Council of States, it was approved by 38 votes to 2, with 4 abstentions.

The implementation of minimum taxation in Switzerland has to be carried out by means of a constitutional amendment. The electorate will vote on this on 18 June 2023.

The OECD/G20 project provides for a minimum tax rate of 15% for large multinational enterprises with annual revenue of at least EUR 750 million, whereby the minimum tax rate must be reached in each jurisdiction. Large multinational enterprises are corporate groups that have a tax connection (subsidiary, permanent establishment, etc.) in at least two jurisdictions. They are major employers: in Switzerland, one in every four employees works for such a company.

Nevertheless, relatively few companies are affected by the reform. According to the Federal Statistical Office, over 600,000 companies are active in Switzerland. Of these, it is estimated that only a few hundred Swiss and a few thousand foreign corporate groups are affected by the OECD/G20 reform. More precise figures are not possible due to a partial lack of data. Nevertheless, it is certain that the vast majority of companies in Switzerland are not directly affected by the reform and will continue to be taxed as before.

The minimum tax rate should also apply in Switzerland to large multinational enterprises with annual revenue of at least EUR 750 million, as envisaged in the OECD/G20 project.

If they are taxed at less than 15% in a given canton, they will have to pay a supplementary tax in the future to make up the difference between the effective tax rate and the minimum tax rate of 15%. This supplementary tax is to be levied and collected by the cantons in the same way as direct federal tax.

75% of the supplementary tax revenue is to go to the cantons and 25% to the Confederation.

In order for the introduction of the minimum tax rate to be possible at all from 2024, the proposal makes provision for the Federal Council to be able to implement it with a temporary ordinance. However, this ordinance will then have to be replaced by a law within six years.

The 75/25 revenue distribution between the cantons and the Confederation is binding only for the ordinance. Parliament may adjust the distribution ratio as necessary when drafting the law.

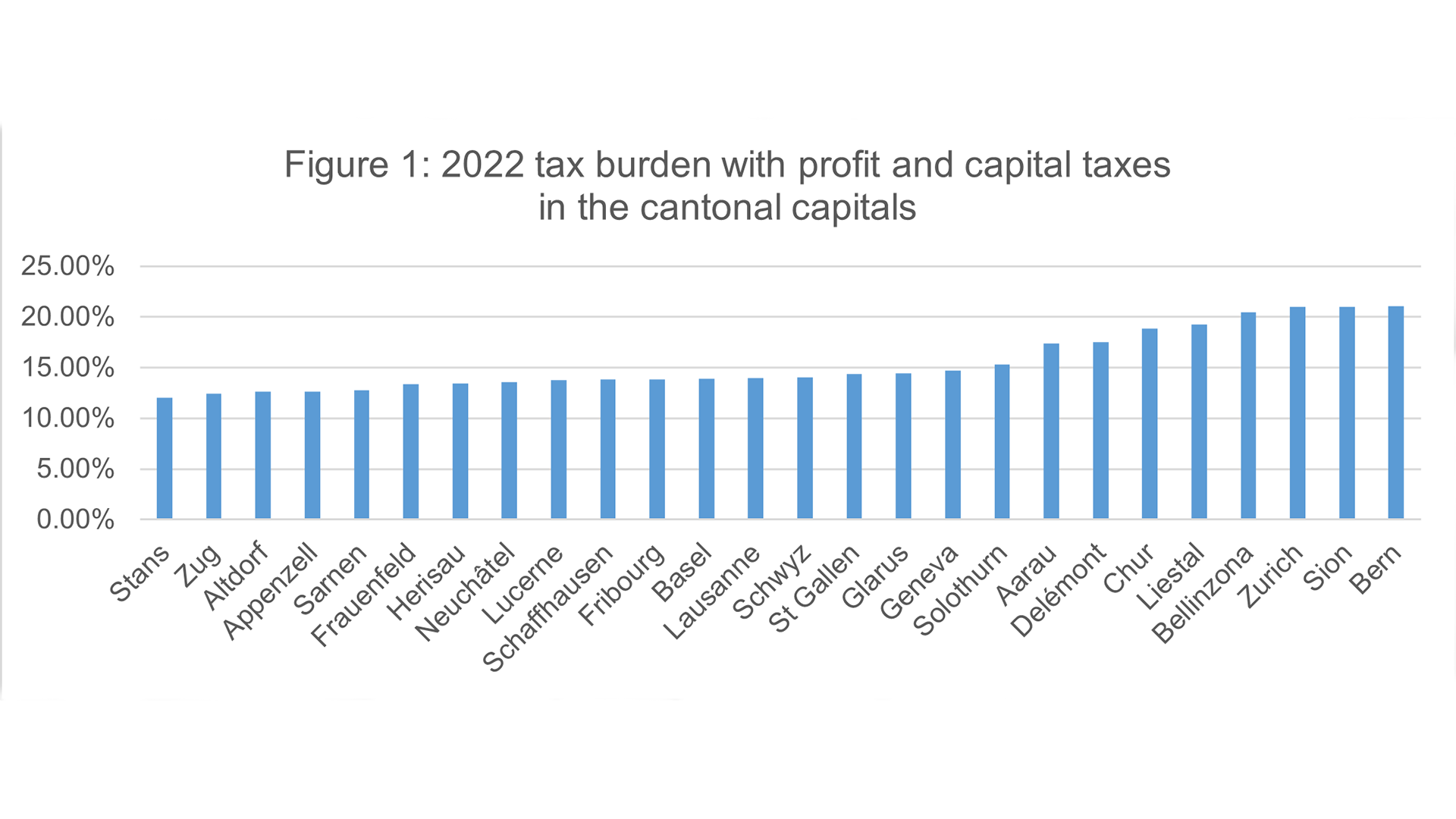

It is currently possible in all cantons for companies to pay less than the OECD minimum tax rate of 15%. On the one hand, many cantons have a relatively low tax burden for all companies (see Figure 1). On the other hand, specific tax concessions, such as those for research and development, can also lead to lower taxation.

The minimum tax rate will generally cause cantons with a very low profit tax burden to lose some of their locational appeal for large multinational enterprises.

The cantons will benefit from the receipts either directly via the supplementary tax or indirectly via national fiscal equalization, which reduces the differences between financially stronger and financially weaker cantons (see also question 6).

Notes: based on a corporate group with a pre-tax net profit of CHF 100 million and capital and reserves of CHF 1 billion in Switzerland. 2021 was used for Frauenfeld.

They will benefit via the fiscal equalization system, as the cantons and the Confederation have to pay a portion of their receipts from the supplementary tax into the fiscal equalization system. An additional third of the federal share will go to fiscal equalization. Financially weaker cantons in particular will benefit from these additional funds in the fiscal equalization system.

It is estimated that the receipts from the supplementary tax will amount to CHF 1-2.5 billion in the first year. These tax receipts may be counteracted by opposing effects in the medium to long term. The OECD/G20 minimum tax rate will make Switzerland less appealing from a tax perspective. This could cause companies to invest less in Switzerland, for example, or to decide not to establish a base in Switzerland.

However, it is difficult to estimate both the short- and long-term financial impact of the supplementary tax. Some reasons for this are as follows:

The limited pool of data: it is not possible, for example, to determine the corporate groups affected, as the existing statistics are based on individual companies rather than on corporate groups.

Different assessment bases: the rules established by the OECD/G20 for the determination of profits differ from those applicable in Switzerland. These differences may lead to higher or lower receipts from the supplementary tax.

Possible behavioural adjustments: since there are no historical empirical values, it is unclear whether other jurisdictions will adjust their tax systems or whether companies will adjust their structures and investments.

If other jurisdictions do not introduce the minimum tax rate of 15%, Switzerland could collect the difference between the lower tax burden in the other jurisdiction and the minimum tax rate. Details of how this mechanism works can be found in the Federal Council dispatch.

75% of the receipts from the supplementary tax will go to those cantons where large multinational enterprises were previously taxed at a rate lower than 15%. The Confederation will receive 25% of the receipts. This distribution ratio decided by Parliament is based on a compromise reached with representatives of the Confederation, the cantons and the communes.

This distribution was chosen so that the receipts can be allocated in a targeted manner where the additional tax burden leads to a loss of locational appeal, i.e. where corporate groups will have to pay higher taxes than at present.

However, there will be a redistribution between all cantons via the national fiscal equalization system. Put simply, the fiscal equalization mechanism will ensure that cantons that receive additional receipts thanks to the supplementary tax have to pay more in favour of the financially weak cantons. The Confederation is also required to pay a third of its share of the additional tax revenue into this resource equalization (see also question 4).

However, the distribution ratio is not set in stone. It is binding only for the ordinance with which the Federal Council can initially introduce the minimum tax rate. Parliament may adjust the distribution ratio if necessary when drafting the law that has to replace the ordinance within six years (see also question 3). In this way, it will be possible to learn from experience with the supplementary tax and make any corrections needed.

The cantons will make sovereign decisions on how they use their receipts from the supplementary tax and on whether to take locational measures. The cantons must take appropriate account of the communes. Cantonal measures must comply with international requirements. In particular, the measures may not constitute prohibited state aid. Furthermore, they should be compatible with the OECD/G20 requirements. Accordingly, direct compensation for the companies affected by the minimum tax rate would not be possible. Any funds must be accessible to all companies that carry out the supported activity, for instance. The promotion of research and development, for example, can create incentives with economic value added.

The Confederation will allocate around a third of its receipts from the supplementary tax to national fiscal equalization. The remaining funds are to be used for measures to foster the locational appeal of Switzerland as a whole. One possible approach would be to strengthen Switzerland's position as a location for education, research and innovation and to counteract the skills shortage in the area of work-life balance. The Federal Council and Parliament will decide on the specific measures.

The OECD/G20 rules on minimum taxation are a so-called common approach. This means that the jurisdictions are not legally obliged to adopt these rules.

However, if they decide to write them into national law, they should follow the model rules and guidance of the OECD/G20. Switzerland, together with many other jurisdictions, has committed to the OECD/G20 rules on minimum taxation.

If Switzerland does not introduce minimum taxation, other jurisdictions could collect the difference between the lower tax burden in Switzerland and the minimum tax rate of 15%. The corporate groups concerned would therefore have to pay the additional taxes abroad instead of in Switzerland. Details of how this mechanism works can be found in the Federal Council dispatch.

The proposal adopted by Parliament created the prerequisites for the minimum tax rate to come into force in Switzerland on 1 January 2024. The Federal Council will decide on its implementation in due course. In doing so, it will take account of developments in other countries. Switzerland also expects its partners in the OECD to introduce the minimum tax rate; it will not rush ahead on its own.

The EU member states agreed in December 2022 that they wish to implement the OECD/G20 minimum tax rate. They have set themselves the target of introducing it from 2024. Other jurisdictions such as the United Kingdom, Canada and Japan have also announced that they will introduce it from 2024.

The United States has launched its own 15% corporate alternative minimum tax (CAMT) for large corporations. The two minimum taxes differ in the following key areas, among others:

Scope: the OECD minimum tax applies to multinational enterprises with annual revenue of at least EUR 750 million; the CAMT applies to multinational corporate groups with average annual adjusted financial statement income exceeding USD 1 billion.

Blending: the OECD minimum tax follows a country-by-country approach, while the CAMT follows a worldwide approach to determine whether the 15% minimum tax is reached.

The relationship between the CAMT and the OECD minimum tax remains unclear.

Switzerland cannot implement minimum taxation without the proposed constitutional amendment. If it does not introduce the minimum tax rate, or does so later than other jurisdictions, those other jurisdictions could collect the difference between the lower tax burden in Switzerland and the minimum tax rate of 15%. As a result, the multinational enterprises concerned would pay the additional taxes abroad rather than in Switzerland.