Published on 20 December 2024

UBS takeover of Credit Suisse

Am 19. März 2023 verabschiedete der Bundesrat ein Massnahmenpaket, das die Übernahme der Credit Suisse durch die UBS ermöglichte.

Brief summary

In March 2023, Credit Suisse was experiencing an acute crisis of confidence. The Federal Council, the SNB and FINMA therefore had to intervene at very short notice in mid-March to protect the Swiss economy and avert any damage to the country. On 19 March 2023, the Federal Council adopted a package of measures that enabled the takeover of Credit Suisse by UBS. Thanks to the swift takeover by UBS and the accompanying government measures, it was possible for the financial system to be stabilised for the long term. The package of measures in connection with the takeover of Credit Suisse by UBS included, among other things, a federal loss protection guarantee for UBS in the amount of CHF 9 billion and a guarantee of CHF 100 billion in favour of the SNB to secure liquidity assistance loans.

On 11 August 2023, UBS announced the termination of the federal loss protection guarantee without replacement. At the same time, it also ended, without replacement, the agreement between Credit Suisse and the SNB on liquidity assistance loans with a federal default guarantee, following full repayment of these loans. The termination of the federal loss protection guarantee and the liquidity assistance loans with a federal default guarantee is final.

The Confederation did not have to assume any losses arising from these guarantees. With the termination of these guarantees, the associated risks also ceased to apply for the Confederation and taxpayers.

Frequently asked questions (FAQ)

The private takeover of Credit Suisse by UBS, supported by a public liquidity back-stop, strengthened confidence in the financial system and created stability for the international financial system, thereby averting serious consequences for the Swiss economy, while at the same time keeping the cost for the state and taxpayers as low as possible. All of the foreign supervisory authorities involved viewed the Swiss authorities' action as appropriate. It also provided reassurance to international financial markets.

The bankruptcy of a systemically important bank like Credit Suisse would have had drastic consequences for Switzerland. Banks in general, but systemically important banks in particular, are key for a national economy to function, as businesses and households depend on them for their economic operations. The failure of a systemically important bank would have ramifications that go beyond the loss of tax contributions or jobs at the bank in question. First, the bank's failure would mean that hundreds of thousands of clients throughout Switzerland – including many SMEs – would lose access to a substantial portion of their bank balances and would quickly find themselves unable to meet their payment obligations. SMEs and households throughout Switzerland would have found it almost impossible to function economically. The Swiss economy would have run the risk of grinding to a halt.

In the case of globally active systemically important banks, there is also a high risk of contagion. The discovery that clients of a globally active systemically important bank are no longer able to access their assets would trigger a loss of confidence both in Switzerland and globally. Other, fundamentally "healthy" banks in Switzerland would be affected. The uncontrolled failure of a globally active systemically important bank could then trigger a global financial crisis.

Liquidity assistance and risks for the Confederation

Despite the bank's own liquidity supply and the SNB's extraordinary liquidity assistance, incidents may occur that can lead to an abrupt loss of confidence in the bank by market participants and thus to liquidity problems. This can be the case even if the bank meets the regulatory capital requirements. The liquidity assistance would also have been necessary under alternative scenarios such as a public takeover.

- CHF 100 billion in additional liquidity assistance loans from the SNB to Credit Suisse and UBS, secured by preferential rights in bankruptcy proceedings for the SNB, but without a state guarantee from the Confederation (= additional emergency liquidity assistance, or ELA+).

- CHF 100 billion in secured liquidity assistance from the SNB, secured by preferential rights in bankruptcy proceedings for the SNB, coupled with strict conditions, and by a state guarantee from the Confederation (= public liquidity backstop). The preferential rights in bankruptcy proceedings and the strict conditions significantly reduced the risk for the Confederation.

- A state guarantee of a maximum of CHF 9 billion for UBS to cover any losses on the sale of specific Credit Suisse assets, consisting essentially of assets that did not fit UBS's strategy. The first CHF 5 billion of any losses on these positions would have been borne by UBS in any case. The loss protection agreement between the Confederation and UBS was terminated with effect from 11 August 2023.

Not part of the package of 19 March 2023:

- CHF 50 billion in emergency liquidity assistance from the SNB. This is an existing SNB monetary policy instrument. Banks can access SNB liquidity against collateral (= emergency liquidity assistance, or ELA). According to its own press release of 16 March 2023, Credit Suisse accessed up to CHF 50 billion under this arrangement.

- CHF 100 billion in additional liquidity assistance loans from the SNB to Credit Suisse and UBS, secured by preferential rights in bankruptcy proceedings for the SNB, but without a state guarantee from the Confederation (= additional emergency liquidity assistance, or ELA+).

In the event of bankruptcy, outstanding loans from the SNB, insofar as these are additional liquidity assistance loans within the meaning of the emergency ordinance, are assigned to the second bankruptcy class and are thus repaid from the bankruptcy estate immediately after the first class (including employee wages, social security contributions). Within the second bankruptcy class, these claims are ranked after privileged liabilities (e.g. social security contributions, privileged deposits), but ahead of the remaining claims in the third bankruptcy class.

The Confederation earned receipts totalling around CHF 200 million from the state-guaranteed liquidity assistance and the loss protection guarantee (40 mn loss protection guarantee, 100 mn PLB commitment premium, 60.6 mn risk premium for the PLB effectively utilised). This covered expenditure incurred by the Confederation for consultancy services provided by external experts in connection with the UBS guarantee.

Internationally, a public liquidity backstop is part of the standard crisis toolkit. It can be a critical prerequisite for a systemically important bank's business continuity. Public liquidity backstops (PLBs) are based on recommendations of the Financial Stability Board (FSB), and have been introduced in different forms in various jurisdictions (e.g. United States, United Kingdom, European Union). The Federal Council had to use an emergency ordinance during the Credit Suisse crisis in March 2023, as Switzerland does not have a PLB anchored in law. In September 2023, the Federal Council adopted the dispatch to Parliament on the introduction of the PLB into ordinary law.

The corresponding agreements were terminated, which means that the Confederation no longer has any financial obligations in the form of guarantee credits. Consequently, the Confederation is no longer exposed to any financial risks in this regard.

Loss protection guarantee

At the beginning of March, Credit Suisse experienced a crisis of confidence. It was no longer able to restore market and client confidence on its own, or to avoid bankruptcy or restructuring. As a result, the Swiss economy also faced unforeseeable upheaval. It was possible for these serious consequences to be averted by UBS taking over Credit Suisse. This takeover emerged as the best overall solution for financial stability and the Swiss economy. The pivotal element was the federal government's willingness to assume any losses on certain assets up to a maximum of CHF 9 billion, provided that UBS shouldered losses of at least CHF 5 billion. The loss protection agreement governed the specifics of this guarantee. The in-depth analysis of the assets acquired through the takeover of Credit Suisse took time. UBS then came to the conclusion that the guarantee was no longer necessary.

After the completion of the takeover of Credit Suisse on 12 June 2023, UBS was better able to assess the actual risk of losses arising from the Credit Suisse assets defined in the loss protection agreement. By terminating the agreement, UBS ceased to benefit from the federal loss protection guarantee for these assets. The Confederation thus achieved its goal of enabling a takeover of Credit Suisse and thereby stabilising the financial centre without burdening the state.

UBS voluntarily decided to terminate the agreement. The loss protection agreement allowed for immediate termination at any time by UBS.

The termination of the loss protection agreement is final. UBS thus voluntarily decided not to avail itself of the federal loss protection guarantee. The legal basis required for the loss protection agreement (Art. 14a of the Federal Council's emergency ordinance of 16 March 2023) was limited until 16 September 2023. The Confederation cannot enter into a new loss protection agreement without a legal basis and without an approved guarantee credit.

The Confederation engaged specialised external consultants in connection with the loss protection agreement with the aim of minimising the risks for the Confederation and the taxpayer as far as possible. The costs of these external consultancy services were more than covered by the set-up fee of CHF 40 million.

UBS paid CHF 40 million in the form of a set-up fee. The first tranche of CHF 20 million was paid at the end of June 2023 and the second tranche at the end of September 2023.

Public liquidity backstop

As of the end of May 2023, Credit Suisse had repaid its outstanding PLB amounts in full to the Swiss National Bank (SNB). The next logical step was to terminate the loan agreement between the SNB and Credit Suisse, and the loss protection agreement between the Confederation and the SNB.

The agreement between the SNB and Credit Suisse was terminated by mutual consent. The termination of the agreements for liquidity assistance loans with a federal default guarantee up to a maximum of CHF 100 billion (public liquidity backstop) meant that the federal guarantee also ceased. The Confederation did not have to make any payments under the guarantee and therefore did not suffer any loss. Upon termination, the Confederation had earned receipts totalling CHF 161.3 million on the default guarantee for the SNB loans to Credit Suisse.

The termination of the PLB agreement is final. Credit Suisse (and UBS as legal successor) thus voluntarily decided not to avail itself of liquidity assistance loans with a federal default guarantee. This means the federal guarantee credit needed for the guarantee ceased to exist. It is not possible to conclude a new guarantee agreement without a guarantee credit.

Somewhat. This dispatch is also intended to simultaneously transfer into ordinary law not only the framework for a PLB instrument as introduced in March 2023 by the Federal Council via ordinance, but also other measures introduced at that time to support the takeover of Credit Suisse by UBS that still appear necessary. The termination of the PLB agreement had no impact on the ordinary part, i.e. the introduction of a PLB instrument. However, the provisions of the ordinance of 16 March 2023 relating to this agreement became obsolete as a result of the termination. Consequently, only certain provisions of the ordinance in connection with the granting of additional liquidity assistance loans (ELA+) were submitted to Parliament as formal legal provisions.

Emergency law

Although the existing TBTF regulations strengthened the capital base and liquidity of systemically important banks, the Federal Council had only sketched out the parameters for a potential state guarantee for liquidity assistance (public liquidity backstop), an instrument that has been tried and tested internationally, and the corresponding legislative project was still in the pipeline at the time of the Credit Suisse crisis. In view of the severe market turmoil Credit Suisse was facing, the Federal Council introduced this instrument based on emergency law under Articles 184 and 185 of the Federal Constitution in order to safeguard the stability of the Swiss economy and the global financial system.

Legislation issued by the Federal Council on the basis of Article 184 paragraph 3 and Article 185 paragraph 3 of the Federal Constitution must always apply for only a limited period. Any emergency ordinance would expire after six months if no dispatch had been submitted to Parliament in the meantime (Art. 7 of the GAOA). For reasons of legal certainty, specific measures taken on the basis of the emergency ordinance continue to apply.

In the case at hand, there were exceptional secrecy considerations, in particular because of trade secrets and ongoing negotiations. It was important that the authorities receive all relevant information from the systemically important banks. The FoIA could have hampered this process, as the affected institutions might have been concerned that the authorities would have had to grant access to the information and documentation provided. This could have resulted in the institutions providing the relevant information in incomplete form or after a long delay, or not providing it at all. In this regard, please refer also to the explanatory report on the ordinance (Art. 6 para. 3).

On 11 August 2023, the federal guarantees and loans issued under the ordinance were terminated. On 6 September 2023, the Federal Council decided to repeal Article 6 paragraph 3 of the emergency ordinance and to refrain from writing the provision into ordinary law.

No. There is no causal link between the statement made by the Head of the FDF and the question of the applicability of emergency law. Furthermore, no such causal link can be inferred from the partial decision of the Federal Administrative Court.

The relevant statement made by the Head of the FDF on 19 March 2023 regarding the takeover of Credit Suisse by UBS was as follows: “This is no bailout. This is a commercial solution.”

This statement is correct and undisputed. It was and is irrelevant to the determination that the merger by absorption of Credit Suisse into UBS was a legal transaction between two private legal entities and not a state recapitalisation or (partial) nationalisation (see also the glossary entry in the PInC report for the term “bailout”).

The extent to which the fact that this was a legal transaction between two private legal entities is decisive for the question of the applicability of emergency law will be the subject of a judicial assessment by the Federal Supreme Court.

Alternative scenarios

On 19 March 2023, there were several options available to solve the acute problems of Credit Suisse, including a takeover by another bank, nationalisation and restructuring in accordance with the TBTF regulations. After careful consideration, however, the Federal Council found the takeover of Credit Suisse by UBS to be the best overall solution for financial stability and the Swiss economy.

The alternatives to a takeover by UBS were:

- Temporary public ownership: temporary public ownership (TPO) of the entire Credit Suisse Group was not at the forefront during the preparatory work for regulatory and legal reasons, as well as due to risk considerations, and it was not pursued as a priority in view of the real possibility of a private takeover. Had the federal government taken over Credit Suisse, it would have had to assume all of the bank's risks and its management.

- Restructuring of the bank as provided for in the TBTF regime, including bail-in to absorb the necessary losses from the subsequent restructuring work: the massive loss of confidence in Credit Suisse was so severe before the weekend of 18 and 19 March that it was highly debatable whether another capital increase and restructuring could have restored the necessary confidence.

- Bankruptcy and triggering of the emergency plan: the bankruptcy of the financial group and the activation of the Swiss emergency plan to ensure the continuity of systemically important functions in Switzerland in particular would have been hugely destabilising for the markets in the prevailing circumstances. Moreover, it would have been extremely unclear whether the separated, surviving Swiss bank would have been able to regain market confidence in the long term in this situation.

- Temporary public ownership: temporary public ownership (TPO) of the entire Credit Suisse Group was not at the forefront during the preparatory work for regulatory and legal reasons, as well as due to risk considerations, and it was not pursued as a priority in view of the real possibility of a private takeover. Had the federal government taken over Credit Suisse, it would have had to assume all of the bank's risks and its management.

The TBTF regulations stipulate that individual legal entities can be declared bankrupt in the event of a bank's impending insolvency. This would entail allowing the entire bank to fail and retaining only those bank functions which are systemically important for Switzerland.

The Federal Council and the supervisory authorities deemed this scenario to be much too risky in the given situation, where global financial markets were in turmoil.

There were two reasons for this:

- First, in the extremely fragile environment at the time, it could have triggered an international financial crisis with massive repercussions for Switzerland as a business location and financial centre.

- Second, client confidence in Credit Suisse had been severely eroded. It would have been unclear whether spinning off the Swiss business arm in this situation would have been able to regain market confidence in Credit Suisse (Schweiz) AG.

- First, in the extremely fragile environment at the time, it could have triggered an international financial crisis with massive repercussions for Switzerland as a business location and financial centre.

Regulation

The TBTF measures (increased capital and liquidity requirements, and improved resolvability) are suitable for lowering the likelihood of state intervention. The stability of the Swiss financial sector as a whole is also attributable to these measures. However, due to massive and rapid outflows of funds, confidence in Credit Suisse was eroded very quickly, despite it having sufficient capital and high liquidity for a prolonged period, and the bank was at risk of bankruptcy. Given the absence of a legal basis for a public liquidity backstop, it had to be enacted under emergency law in order to safeguard the stability of the Swiss economy and the financial system.

The existing regulations will be continually reviewed and, if necessary, adapted to new developments. Specifically, in September 2023, the Federal Council adopted the dispatch to Parliament on the introduction of a public liquidity backstop into ordinary law. Moreover, the Federal Council brought higher liquidity requirements into force on 1 July 2022 for systemically important banks.

At the end of March 2023, the Federal Council decided to review the takeover of Credit Suisse by UBS and too evaluate the TBTF regulatory framework. The Federal Council based its decision on Article 52 of the Banking Act, according to which it is required to report regularly on systemically important banks. The next such report is due to be presented by the beginning of April 2024.

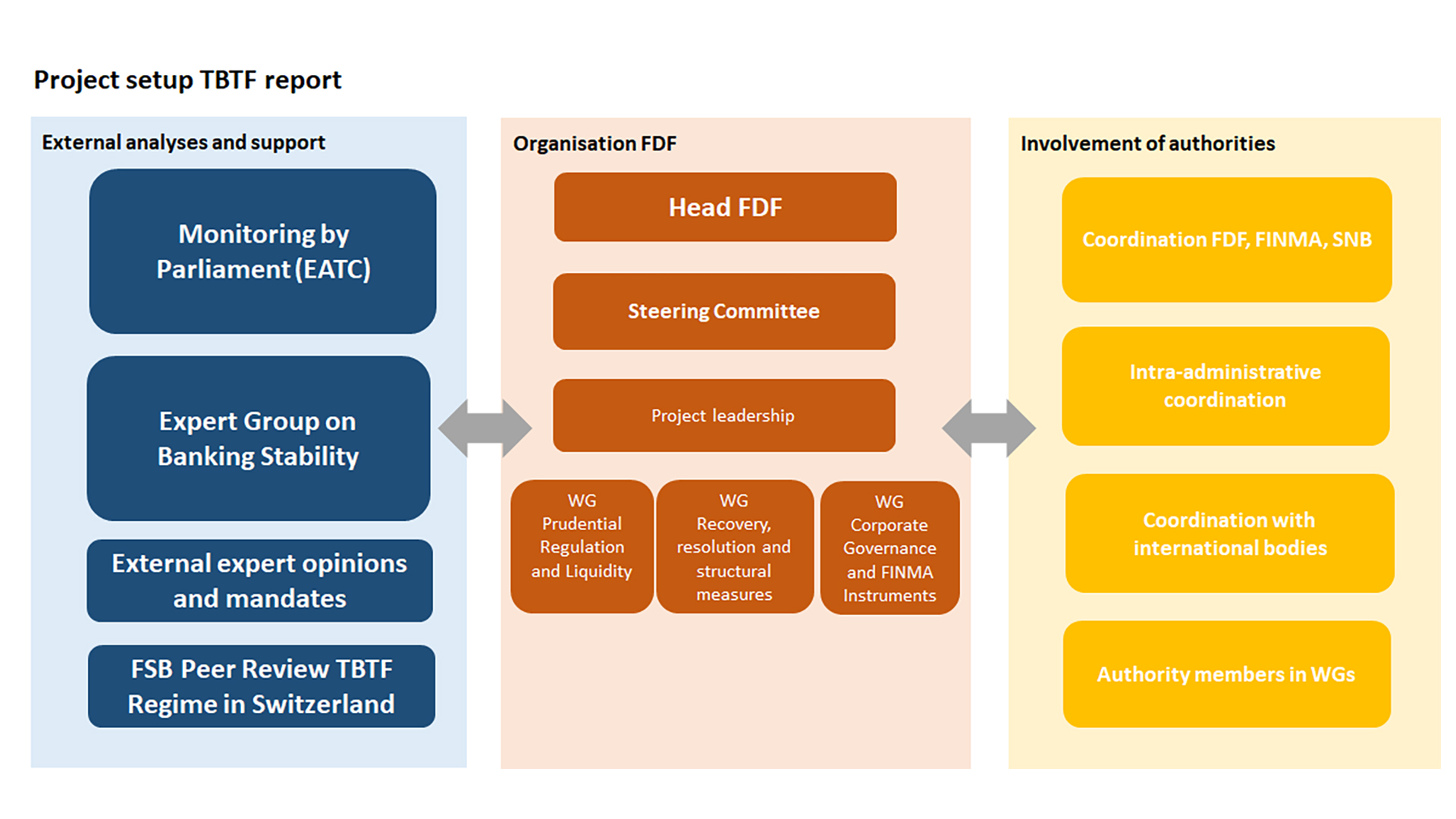

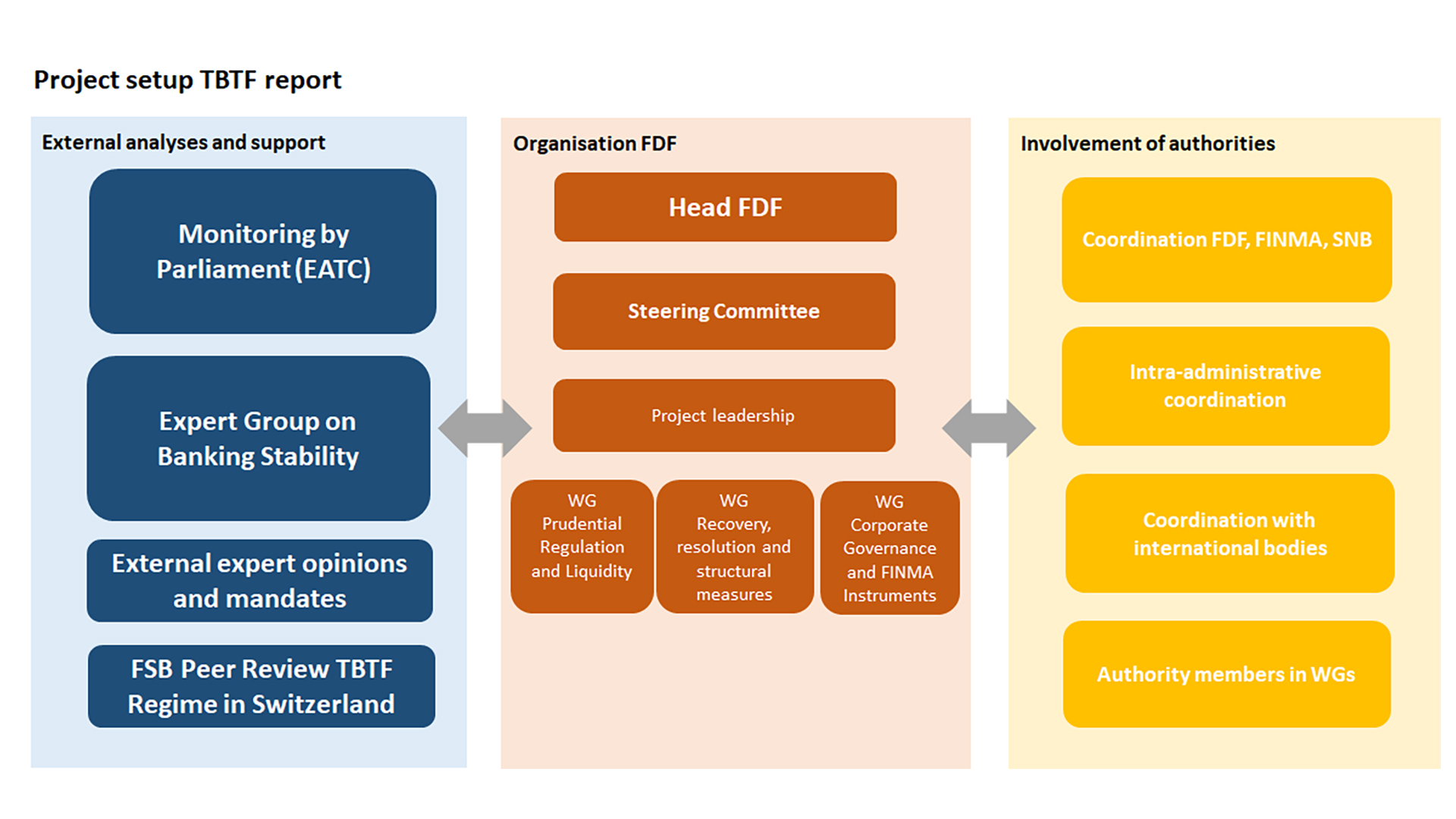

In connection with the preparation of the report, the Federal Department of Finance (FDF) established a working group: the expert group on banking stability submitted its report as mandated by the FDF. The report was published on the FDF website on 1 September 2023. The report's findings are being incorporated into the FDF's ongoing work for the attention of the Federal Council.

{kind=link}

Consequences for third parties

Credit Suisse dividend payments were not allowed for the duration of the state support. The Federal Council also imposed restrictions with regard to remuneration packages, pursuant to Article 10a of the Banking Act.

Yes. FINMA was provided with a clearer legal basis so that part of Credit Suisse's regulatory capital could be written off (private creditors are to share in the exposures to the tune of CHF 16 bn1). This ensured that private measures were taken in addition to state measures.

1 Correction of 20.03.2023: changed from "around CHF 17 bn" to "CHF 16 bn"

Yes, deposits of up to CHF 100 000 are safe, even if the bank were to go bankrupt. The takeover of Credit Suisse by UBS and the public liquidity backstop boosted confidence in the bank's stability.

There are no indications of this happening in Switzerland to date. However, the relevant regulations and instruments are in place.

Employees and wages

As instructed by the Federal Council, the FDF issued an order stating that the variable remuneration still outstanding as at 23 May 2023 for the top three levels of management at Credit Suisse was to either be cancelled in full (Executive Board), reduced by 50% (members of management one level below the Executive Board) or reduced by 25% (members of management two levels below the Executive Board). This took account of the most senior managers' responsibility for the situation at Credit Suisse in a differentiated manner. Credit Suisse was also obliged to examine the possibility of recovering variable remuneration already paid out and to report to FINMA and the FDF on the matter. In addition, the variable remuneration due in 2023 was cancelled or reduced on a pro rata basis until the completion of the takeover. These measures affected around 1,000 employees and concerned CHF 62 million in variable remuneration.

The federal guarantee was not required because UBS got into difficulty; instead, it was provided proactively to enable a solution to be found for Credit Suisse. If UBS could no longer offer a competitive remuneration system, there would have been a danger of this resulting in a considerable risk for operational stability and ultimately for the bank's entire business, which was something to be avoided.

However, UBS was required to establish a separate organisational unit for winding down the portfolio. Within this organisational unit, there was an obligation to implement incentive-based remuneration schemes for the employees charged with the realisation. The assets were to be managed in such a way that losses were minimised and realisation proceeds were maximised.

Figures overview

Definitive status as of 31 December 2023

State-guaranteed liquidity assistance loan provided to Credit Suisse (public liquidity backstop, PLB)

Commitment premium of 0.25% p.a. for CHF 100 billion public liquidity backstop:

- Accrued premium (cumulative 19 March 2023 to 11 August 2023): CHF 100.7 million

Risk premium of 1.5% p.a. for effectively utilised public liquidity backstop

- Accrued premium payments (cumulative 20 March 2023 to 30 May 2023): CHF 60.6 million

In addition to the commitment and risk premia payable to the Confederation, Credit Suisse paid the SNB interest and a risk premium.

The other liquidity assistance provided by the SNB (without a state guarantee) is not mentioned here.

UBS loss protection guarantee: guarantee fee

Initial set-up fee:

- CHF 40 million (in two instalments of CHF 20 million each)

The federal government's expenses for the UBS loss protection guarantee (external consultancy) totalled CHF 3.3 million.

The following did not apply due to the termination of the agreement on 11 August 2023:

- Annual maintenance fee of 0.4% on CHF 9 billion, i.e. CHF 36 million p.a. (from October 2023)

- Annual drawn portion fee of between 0% and 4% on CHF 9 billion, contingent on the losses already realised and those still to be expected

Documentation

Special dispatch on guarantee credits

22 April 2026

Too-big-to-fail regulations: Federal Council adopts dispatch and Capital Adequacy Ordinance

During its meeting on 22 April 2026, the Federal Council adopted the dispatch on the revision of the Banking Act. In the future, systemically important banks in Switzerland will have to fully back their participations in foreign subsidiaries with Common Equity Tier 1 (CET1) capital. This targeted measure is key to strengthening financial stability. Parliament will be able to debate the legislative proposal from summer 2026. At the same time, the Federal Council amended the Capital Adequacy Ordinance. The amendments concern the capital backing for certain balance sheet items such as software, and will come into force on 1 January 2027. The solution proposed by the Federal Council is more moderate than planned, due to the results of the consultation procedure. In terms of capital requirements, the result is thus a balanced overall package that takes account of the comments received.

26 September 2025

Federal Council launches consultation on the capitalisation of foreign participations by parent companies of systemically important banks

During its meeting on 26 September 2025, the Federal Council launched the consultation on amendments to the Banking Act and the Capital Adequacy Ordinance. Under the amendments, systemically important banks in Switzerland would be required to provide full capital backing for their participations in foreign subsidiaries in future. The capital requirement will be raised in increments over a seven-year period. The consultation will last until 9 January 2026.

6 June 2025

Federal Council draws lessons from Credit Suisse crisis and defines measures for banking stability

The review of the Credit Suisse crisis showed that the too big to fail regime needs to be improved in order to reduce risks for the state, taxpayers and the economy. For this reason, during its meeting on 6 June 2025 the Federal Council determined the parameters for the corresponding amendments to acts and ordinances, which will be submitted for consultation in stages from this autumn onwards. These include stricter capital requirements for systemically important banks with foreign subsidiaries, additional requirements on the recovery and resolution of systemically important banks, the introduction of a senior managers regime for banks and additional powers for the Swiss Financial Market Supervisory Authority (FINMA). The Federal Council also opened a consultation process for those measures that are to be implemented directly at ordinance level.The review of the Credit Suisse crisis showed that the too big to fail regime needs to be improved in order to reduce risks for the state, taxpayers and the economy. For this reason, during its meeting on 6 June 2025 the Federal Council determined the parameters for the corresponding amendments to acts and ordinances, which will be submitted for consultation in stages from this autumn onwards. These include stricter capital requirements for systemically important banks with foreign subsidiaries, additional requirements on the recovery and resolution of systemically important banks, the introduction of a senior managers regime for banks and additional powers for the Swiss Financial Market Supervisory Authority (FINMA). The Federal Council also opened a consultation process for those measures that are to be implemented directly at ordinance level.

23 May 2025

Variable remuneration at Credit Suisse: the Confederation appeals to the Federal Supreme Court

The Federal Department of Finance is contesting the decision of the Federal Administrative Court (FAC), which found that the reduction or cancellation of variable remuneration for former members of Credit Suisse management was illegal. The FDF has decided to lodge an appeal with the Federal Supreme Court, which will make a final decision on the matter.

20 December 2024

Federal Council issues opinion on report of Parliamentary Investigation Committee concerning Credit Suisse

The Federal Council has taken note of the report prepared by the Parliamentary Investigation Committee (PInC) on "Management by the authorities – CS emergency merger". It welcomes the fact that the PInC's report takes a positive view of the authorities' actions in the Credit Suisse crisis and of the solution chosen with the takeover by UBS. In its report for the attention of the Federal Assembly, the Federal Council sets out its position on the PInC's recommendations, motions and postulates. The work carried out by the PInC largely confirms the expediency of the measures envisaged in the Federal Council's report on banking stability of 10 April 2024.

21 August 2024

Interim solution for withholding tax on too-big-to-fail instruments

During its meeting on 21 August 2024, the Federal Council approved a temporary extension of the special rules on withholding tax for too-big-to-fail (TBTF) instruments to 31 December 2031. This ensures that banks can continue to obtain capital from within Switzerland on competitive terms, thereby contributing to financial stability. At the same time, the temporary nature of the extension ensures that the legislator is able to formulate a definitive regulation as part of the overall package of TBTF measures.

10 April 2024

Banking stability: Federal Council wants to close gaps in too-big-to-fail regulation

Based on Article 52 of the Banking Act and mandates from Parliament, the Federal Council has carried out an in-depth assessment of the regulation of systemically important banks. During its meeting on 10 April 2024, it adopted the associated report on banking stability. The comprehensive review of the Credit Suisse crisis has revealed that the existing too-big-to-fail regime must be developed further and strengthened, in order to reduce the risks to the economy, the state and the taxpayer. The Federal Council is proposing a broad package of measures in this regard. Implementation should also take into account the findings of the Parliamentary Investigation Committee (PInC).

6 September 2023

Federal Council adopts dispatch on introduction of a public liquidity backstop for systemically important banks

During its meeting on 6 September 2023, the Federal Council adopted the dispatch on the introduction of a public liquidity backstop (PLB) for systemically important banks. The Federal Council had already decided on the key parameters for a PLB to strengthen the stability of the financial sector in March 2022. In March 2023, the PLB was put into force by ordinance as part of the takeover of Credit Suisse by UBS. The PLB and certain provisions of the ordinance that are still required are now to be transferred into ordinary law.

1 September 2023

Report of the group of experts on banking stability

Publication Notice

11 August 2023

Credit Suisse/UBS: all federal guarantees terminated

UBS has definitively terminated the agreement regarding the federal loss protection guarantee in the amount of CHF 9 billion, as well as the agreement with the SNB regarding the federal guarantee of no more than CHF 100 billion to secure liquidity assistance loans. These measures, which were created under emergency law to preserve financial stability, will thus cease to exist, and the Confederation and taxpayers will no longer bear any risks arising from these guarantees. Furthermore, the Confederation earned receipts of around CHF 200 million on the guarantees.

9 June 2023

Confederation and UBS sign loss protection agreement

UBS has announced that it will probably complete the Credit Suisse takeover on 12 June 2023. The takeover was the key component of the Federal Council's overall package of 19 March to safeguard financial stability and thus avert damage to the Swiss economy. To make the takeover possible, the federal government provided UBS with a guarantee for potential losses incurred on the realisation of Credit Suisse assets. The loss protection agreement was signed on 9 June 2023. The guarantee will take effect only if the losses arising from the realisation of these assets exceed CHF 5 billion. It is limited to a total of CHF 9 billion. The priority for the federal government and UBS is to minimise potential losses and risks so that recourse to the federal guarantee is avoided to the greatest extent possible. The Federal Council was informed of the loss protection agreement during its meeting on 9 June 2023.

5 June 2023

Group of experts on banking stability now under leadership of Yvan Lengwiler

Yvan Lengwiler has taken over the leadership of the group of experts on banking stability set up by the Federal Department of Finance (FDF). The previous president, Jean Studer, has left the expert group and Rudolf Sigg, the former Chief Financial Officer of Zürcher Kantonalbank, has joined.

25 May 2023

Federal Council initiates consultation on introduction of a public liquidity backstop for systemically important banks

On 24 May 2023, the Federal Council decided that the consultation on the introduction of a public liquidity backstop (PLB) for systemically important banks (SIBs) would be initiated on 25 May 2023. This draft is intended to simultaneously transfer into ordinary law not only the framework for a PLB instrument as introduced in March 2023 by the Federal Council via ordinance, but also other measures introduced at that time and aimed at supporting the takeover of Credit Suisse by UBS. The consultation period, which has been shortened owing to the urgency, will last until 21 June 2023.

23 May 2023

FDF orders measures on remuneration at CS and UBS

The Federal Department of Finance (FDF) has issued an order cancelling or reducing the outstanding variable remuneration of the top levels of management at Credit Suisse. At the same time, the FDF has instructed UBS to design its remuneration system for the employees responsible for the realisation of the Credit Suisse assets covered by the federal guarantee such that the system provides an incentive to achieve the fewest losses possible on the realisation of those assets.

17 May 2023

Federal Department of Finance convenes group of experts on banking stability

On 17 May 2023, the Head of the Federal Department of Finance (FDF), Karin Keller-Sutter, informed the Federal Council that the group of experts on banking stability had been convened. By mid-August 2023, the group of experts, led by Jean Studer, former President of the Bank Council of the Swiss National Bank (SNB), will present the FDF with independent strategic considerations on the role of banks and the framework conditions at federal level with regard to the stability of the Swiss financial centre.

19 April 2023

Federal Council discusses outcome of extraordinary session

At its meeting of 19 April 2023, the Federal Council acknowledged that the National Council had twice rejected the emergency guarantee credits for the Swiss National Bank (SNB) and UBS during the extraordinary session of 11/12 April 2023. Parliament debated these credits on the premise that a rejection would have no legal effect on the Confederation's emergency commitments made to the SNB and UBS. The Federal Council shares this legal opinion. Without these commitments, the takeover of Credit Suisse by UBS, and thus the stabilisation of the financial system, would not have been possible. However, the Federal Council will give the fullest consideration to Parliament's position in its future work and decisions.

5 April 2023

Federal Council makes decisions on variable remuneration at Credit Suisse and UBS

During its meeting on 5 April 2023, the Federal Council instructed the Federal Department of Finance (FDF) to cancel, or reduce by 50% or 25%, all outstanding variable remuneration for the top three levels of management at Credit Suisse. The bank also has to examine whether variable remuneration already paid out can be recovered, and report to the FDF and FINMA on the matter. UBS is obliged to ensure that its remuneration system continues to give appropriate consideration to risk awareness and includes as a criterion the successful, i.e. most profitable possible, realisation of the Credit Suisse assets covered by the state loss guarantee.

21 March 2023

Federal Council makes decisions on variable remuneration at Credit Suisse

The Federal Council has acknowledged that the Federal Department of Finance (FDF) is temporarily suspending certain forms of variable remuneration for Credit Suisse employees by means of an order to the bank. This measure relates to already granted but deferred remuneration for the financial years up to 2022, for example in the form of share awards. Moreover, the Federal Council has instructed the FDF to propose further measures on variable remuneration for the financial years up to 2022 and thereafter. It based this on the decisions already taken last week.

19 March 2023

Safeguarding financial market stability: Federal Council welcomes and supports UBS takeover of Credit Suisse

The Federal Council welcomes the planned takeover of Credit Suisse by UBS. To strengthen financial market stability until the takeover is complete, the federal government is providing a guarantee for additional liquidity assistance from the Swiss National Bank (SNB) to Credit Suisse. This support is intended to secure the liquidity of Credit Suisse and thus also ensure the successful implementation of the takeover. The Federal Council is taking this measure in order to protect financial stability and the Swiss economy.

3 June 2022

Systemically important banks: Federal Council adopts amendments to Liquidity Ordinance

During its meeting on 3 June 2022, the Federal Council adopted amendments to the Liquidity Ordinance. The revision is intended to ensure that systemically important banks hold sufficient liquidity to absorb liquidity shocks and cover their needs in the event of restructuring or liquidation. A high level of liquidity is also a key condition for the introduction of a public liquidity backstop envisaged by the Federal Council. The amended Liquidity Ordinance will enter into force on 1 July 2022.

11 March 2022

Federal Council wants to introduce new tool to strengthen financial sector stability

The Federal Council is planning to expand its toolkit to strengthen the stability of the financial sector. At its meeting on 11 March 2022, it defined key parameters for a "public liquidity backstop", which would allow the Confederation and the Swiss National Bank (SNB) to bolster the liquidity of a systemically important bank that is in the process of resolution. The Federal Department of Finance (FDF) is to prepare a consultation draft by mid-2023.

Media conference of the 19th March 2023

Fact sheets

State Secretariat for International Finance SIF

Bundesgasse 3

Switzerland - 3003 Bern