Federal Council report on banking stability

Based on Article 52 of the Banking Act and mandates from Parliament, the Federal Council has carried out an in-depth assessment of the regulation of systemically important banks.

Strengthen the too-big-too-fail regulation (TBTF)

Based on Article 52 of the Banking Act and mandates from Parliament, the Federal Council has carried out an in-depth assessment of the regulation of systemically important banks. During its meeting on 10 April 2024, it adopted the associated report on banking stability. The comprehensive review of the Credit Suisse crisis has revealed that the existing too-big-to-fail regime must be developed further and strengthened, in order to reduce the risks to the economy, the state and the taxpayer. The Federal Council is proposing a broad package of measures in this regard. Implementation should also take into account the findings of the Parliamentary Investigation Committee (PInC).

Focus areas

In its report in accordance with Article 52 of the Banking Act, the Federal Council has now evaluated the existing too-big-to-fail regime, based on a broad set of internal and external expert opinions. It concludes that many of the measures already introduced at national and international level to increase financial stability have generally proved their worth. However, the assessment also revealed gaps in the existing regime, and thus a need for action to further develop and strengthen regulation. In addition, the Federal Council has used this report to address referred or pending parliamentary procedural requests.

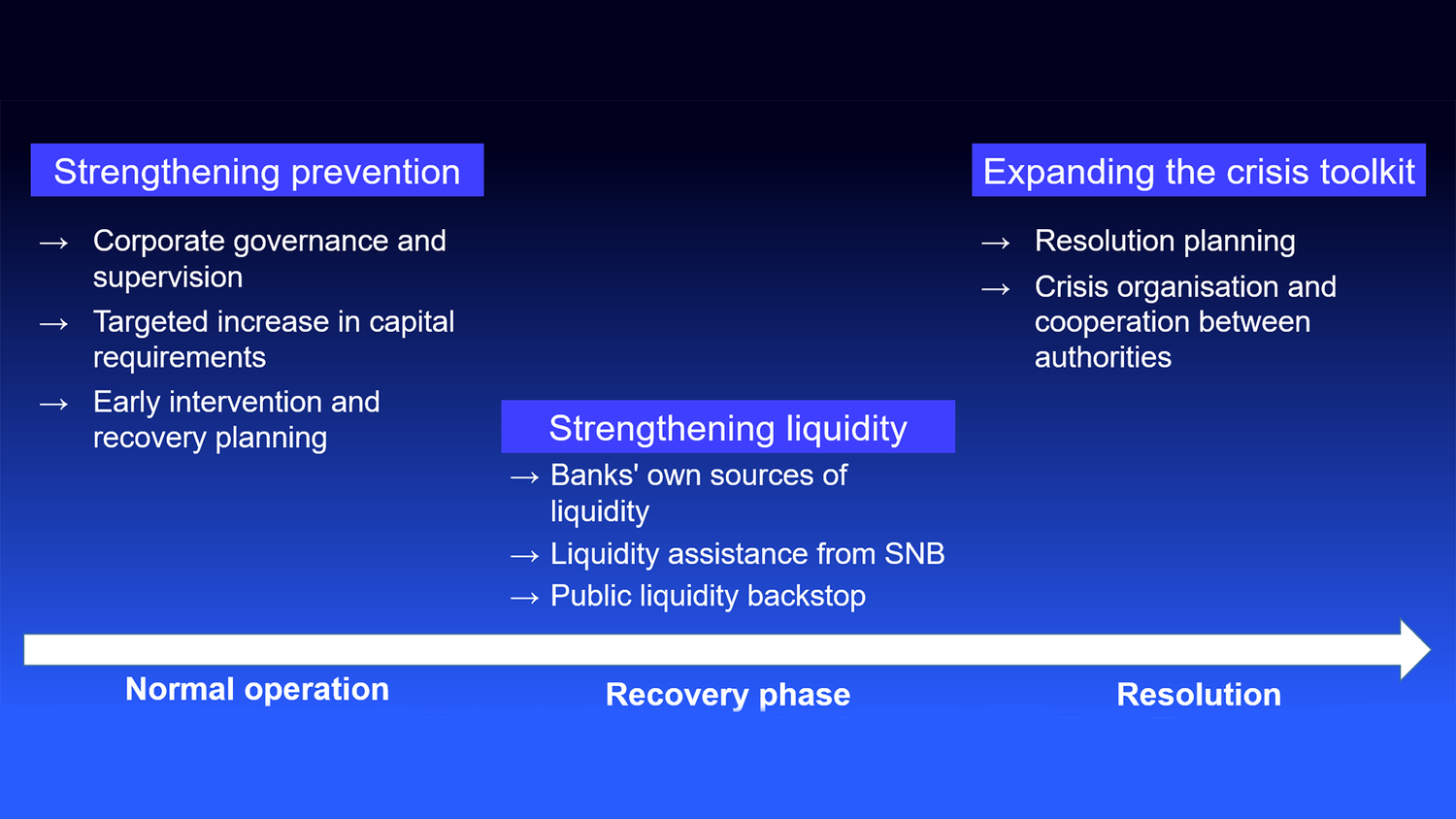

The Federal Council is proposing a package of 22 measures for direct implementation, with a view to strengthening and further developing the too-big-to-fail regime. Seven other measures are to be examined in greater depth. Implementation of the package should significantly reduce the likelihood that another systemically important bank in Switzerland will experience a severe crisis and that emergency measures by the state will be necessary. Moreover, in the event of a crisis, the resolvability of a systemically important bank as a credible option should be ensured. In this way, the Federal Council wants to minimise the risks and costs for the state, the economy and the taxpayer. The Federal Council's package of measures is divided into three focus areas:

- Strengthening prevention: Explicit regulatory requirements and an expanded toolkit for the Swiss Financial Market Supervisory Authority FINMA should be used to impose good corporate governance and more accountable risk management on the part of systemically important banks. This includes a senior managers regime (clear allocation of responsibilities) and rules on bonuses (such as retention periods and clawbacks). The introduction of powers for FINMA to impose fines is being examined. In addition, the quantitative and qualitative capital requirements for systemically important banks should be tightened in a targeted way and supplemented with a forward-looking component. This should strengthen the capital base and improve resolvability. Finally, FINMA's options and duties with regard to early intervention should be expanded.

- Strengthening liquidity: The strengthening of systemically important banks' own liquidity holdings has already been implemented in legislation that came into force in January 2024. In addition, the potential for liquidity provision by the Swiss National Bank should be significantly expanded. Furthermore, the possibility of a public liquidity backstop as part of a potential restructuring of a systemically important bank should be enshrined in ordinary law, as already proposed to Parliament by the Federal Council in September 2023.

- Expanding the crisis toolkit: In a crisis, systemically important banks must be able to exit the market in an orderly manner. In order to strengthen resolvability, resolution planning should be expanded and the legal risks associated with implementation should be further reduced. The crisis organisation and the cooperation between the authorities should also be strengthened and more clearly defined where necessary.

Measures to strengthening the financial stability

Strengthening prevention: Corporate governance and supervision, Targeted increase in capital requirements, Early intervention and recovery planning

Strengthening liquidity: Banks' own sources of liquidity, Liquidity assistance from SNB, Public liquidity backstop

Expanding the crisis toolkit: Resolution planning, Crisis organisation and cooperation between authorities

Press conference

Press release

Banking stability: Federal Council wants to close gaps in too-big-to-fail regulation

Bern, 10.4.2024 - Based on Article 52 of the Banking Act and mandates from Parliament, the Federal Council has carried out an in-depth assessment of the regulation of systemically important banks. During its meeting on 10 April 2024, it adopted the associated report on banking stability.